How Robust Are House Prices in the UK Property Market?

As we plunged into lockdown back in March, it seemed a given that the UK property market would take a significant downturn. Economic uncertainty rarely bodes well for house prices, after all.

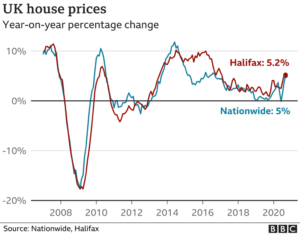

It was surprising, therefore, that house prices have risen so dramatically post-lockdown. The latest House Price Index release from the Office of National Statistics pegs average house price growth at 2.3% in July this year. The following month, Nationwide building society said it saw the highest monthly price rise for 16 years in August, as the average price of a property rose 2% from the previous month. In September, average house prices jumped 1.6% again, according to figures from mortgage lender Halifax, lifting annual growth to 7.3% – the highest since June 2016.

“Few would dispute that the performance of the housing market has been extremely strong since lockdown restrictions began to ease in May,” said Halifax Bank Managing Director Russell Galley. “Across the last three months, we have received more mortgage applications from both first-time buyers and home movers than any time since 2008.”

(Image source: bbc.co.uk)

But how sustainable are these trends? Undoubtedly, the UK property market is experiencing a mini boom – but how long will it last?

We examine the evidence below.

Why Is the UK Property Market So Buoyant Right Now?

The Financial Times’s description of the UK property market as “defying gravity” couldn’t be more apt. Whilst other industries run into struggle after struggle, the housing market seems to have bucked this trend.

Part of this can be put down to pent-up demand. Buying a home was impossible between March and May due to lockdown restrictions. Those that wanted to make a move then but weren’t able to are now actively looking to buy.

Meanwhile, those on the fence about moving will have been encouraged to enter the market by the UK Government’s stamp duty holiday, which was introduced in July and will be in place until March 2021.

As Robert Gardner, Nationwide’s Chief Economist, puts it, “The rebound reflects a number of factors. Pent-up demand is coming through, with decisions taken to move before lockdown now progressing,” he said, adding that Rishi Sunak’s stamp duty holiday affecting properties up to £500,000 in England and Northern Ireland was “adding momentum” by bringing purchases forward. “Behavioural shifts may also be boosting activity as people reassess their housing needs and preferences as a result of life in lockdown,” Gardner said.

A Reassessment of Life Priorities

In a recent article for City AM, Garrington Property Finders Chief Exec Jonathan Hopper explains how the pandemic’s social effects have affected the housing market: “Prices are rising fastest among coastal and country properties as buyers aiming for a new work-life balance built around less commuting seek more green space, fresh air and better value.”

The pandemic has indeed provided plenty of opportunity for reassessing life priorities. Estate agents have reported a surge in people moving to be closer to family for example, or from cities into green-belt areas with plenty of outside space. This has created a surge in demand that has impacted house prices across the board – though particularly in rural and semi-rural areas.

Additionally, due to the surge in remote working, a home office has become a “hot commodity”, according to James Forrester, Managing Director of estate agent Barrows and Forrester. Hopper concurs, saying that an additional bedroom that can be converted into a workspace has moved from being a “nice to have” to a “need to have”.

“Coastal and country properties are the most in demand, but the space race is universal,” he said. “A home office – or at least an extra bedroom that can be used as one – has become a fundamental requirement for thousands of househunters.”

Is This Rise in House Prices Sustainable?

You’ll notice that some of the factors that are driving UK house price growth are temporary.

“Pent-up demand” won’t be pent up forever, and the stamp duty cut will end next March. And whilst we might see the trend towards remote working continue to rise over the mid- to long-term, it’s still safe to assume that at least some people will resume commuting to and from their workplace (and will have a less flexible housing budget as a result).

The temporary nature of these factors makes it likely that we’re currently experiencing a ‘mini boom’ driven by short-term demand.

How Will Further Developments Impact the Housing Market?

The possibility of a boom and bust scenario is also increased by uncertainties around how the furlough scheme will develop. Firms hit hard by the pandemic may find it difficult to continue to employee furloughed workers, resulting in heightened levels of unemployment.

This coincides with the ban on private landlords evicting tenants being lifted in September. It’s possible that private landlords who have served evictions will end up struggling to fill empty properties and opt to sell, thereby easing demand and contributing towards decreased house prices in the medium- to long-term.

Combined with the uncertainty generated by the UK leaving the EU in January 2021, this could cause the market to drop significantly – whether that means a gradual easing off to pre-COVID levels or a heavier crash is hard to say at this point.

That said, the UK Government has proved willing to roll out support for the housing market when needed. It’s not beyond the realms of possibility they would do it again, but precisely what this would look like is hard to predict. And it’s this lack of certainty that, ultimately, means we can’t describe the UK property market as ‘robust’ without some serious reservations.

Strong currently? Absolutely.

Robust in the medium- to long-term? The jury’s still out.

How Stable Is the UK Property Market at the Local Level?

How localised property markets are likely to fare going forward also makes the question of ‘robustness’ a tricky one. How the tier system, regional lockdowns and any potential national actions will affect local house prices is difficult to predict at the moment.

Property experts had thought that affluent, in-demand areas might suffer the least disruption, for example – although the continuation of the furlough scheme raises questions about potential downturns in white-collar areas, too. Meanwhile, a continued shortage of mortgage lending options for low-deposit buyers – and caution on the part of lenders to grant mortgage approvals for this group – could combine with the factors above to hit cheaper areas hard.

See Your Agents Through Unpredictable Times with Sprift

As we enter a long period of unpredictability for the housing market, it’s never been more important to keep one step ahead of market trends in your area.

Until now, market data has been difficult, slow and expensive to access, making in-depth local property market analysis inaccessible for all but the largest estate agencies.

That’s where Sprift comes in.

Sprift grants your agents instant, affordable access to all UK property market data and distils it into a range of hyper-local, Big Data-driven reports to help you sell properties faster, win valuations and beat out the competition.

Sign up for a no-obligation free trial of Sprift today.